L’Or et autres métaux précieux Africains à l’Ère Numérique : Une Révolution Nommée SyncGOLD

👥 À l’attention de :

Orpailleurs, coopératives minières, acheteurs, vendeurs, intermédiaires honnêtes, investisseurs et toute la chaîne de valeur des métaux précieux en Afrique.

📖 Notre Histoire Commence Par un Constat Douloureux

Pendant des générations, l’or africain a été extrait avec courage et sueur.

Des hommes et des femmes se battent chaque jour entre la Côte d’Ivoire, le Mali, le Burkina Faso, le Ghana, le Togo, RDC, RCA…

Mais trop souvent, ces métaux précieux ne profitent pas pleinement à ceux qui le font naître.

Pourquoi ?

Parce que entre la mine artisanale et le marché, s’intercalent :

🔸 Une multitude d’intermédiaires,

🔸 Des risques d’arnaques et d’escroqueries,

🔸 Des retards de paiement,

🔸 Des avances de fonds non sécurisées,

🔸 Des coûts de transport, de sécurité et de stockage élevés.

Résultat ?

Une richesse qui s’évapore avant d’atteindre ses premiers créateurs.

⚡ Et Si l’Or Pouvait y Circuler Aussi Facilement Qu’un Message ?

Aujourd’hui, la révolution est là.

SUREBANQA a créé SyncGOLD : le premier jeton numérique africain adossé à de l’or physique, gramme pour gramme.

SyncGOLD, c’est :

✅ De l’or tangible, stocké sécurisé et auditable en temps réel

✅ Un jeton numérique transférable en quelques secondes, sans intermédiaire inutile.

✅ Une monnaie stable qui ne se dévalue pas, indexée sur la valeur réelle de l’or.

✅ Un passeport financier pour dépenser, échanger, épargner, bref être inclus financierement partout.

🛠 Comment Ça Marche ? Une infrastructure Complete Vous Attend :

1. TOKENISEZ/ACHETEZ de l’or physique en numérique (SyncGOLD) sur XENN, avec vos FCFA, Euros, Dollars, ou même du BTC/ETH.

2. VENDEZ ou RETIREZ en cash via le réseau d'Agent SWAPPIFI/AFROTELLER/LOOP, présent partout dans le monde.

3. DÉPENSEZ avec une carte Visa/Mastercard physique ou virtuelle, même dans votre boutique locale.

4. ÉPARGNEZ en or, à l’abri de l’inflation.

5. ÉCHANGEZ entre devises (FCFA, €, $, Naira) sans frais cachés.

🌟 Pour Les Acteurs de la Filière, Voici Ce Qui Change :

Pour l’orpailleur ou la coopérative :

→ Vendez votre or contre des SyncGOLD immédiatement, sans attendre.

→ La valeur est sécurisée, et vous pouvez la convertir en cash quand vous voulez, où vous voulez.

Pour l’acheteur ou le négociant :

→ Plus besoin de transporter de grosses sommes ou de risquer des transactions opaques.

→ Achetez de l’or tokenisé, livrable physiquement si besoin, avec une traçabilité blockchain.

Pour l’intermédiaire intègre :

→ Travaillez sur une plateforme formalisée, sécurisée et transparente.

→ Fini les avances risquées : les transactions sont instantanées et garanties.

→ Bénéficiez d’avantages concrets (cashback, compte marchand, carte de débit).

🚀 Au-Delà de SyncGOLD : L’Écosystème SUREBANQA Vous Porte

· XENN : Pour créer et gérer vos propres actifs numériques.

· SWAPPIFI : Pour le change et les retraits en espèces à travers l’Afrique.

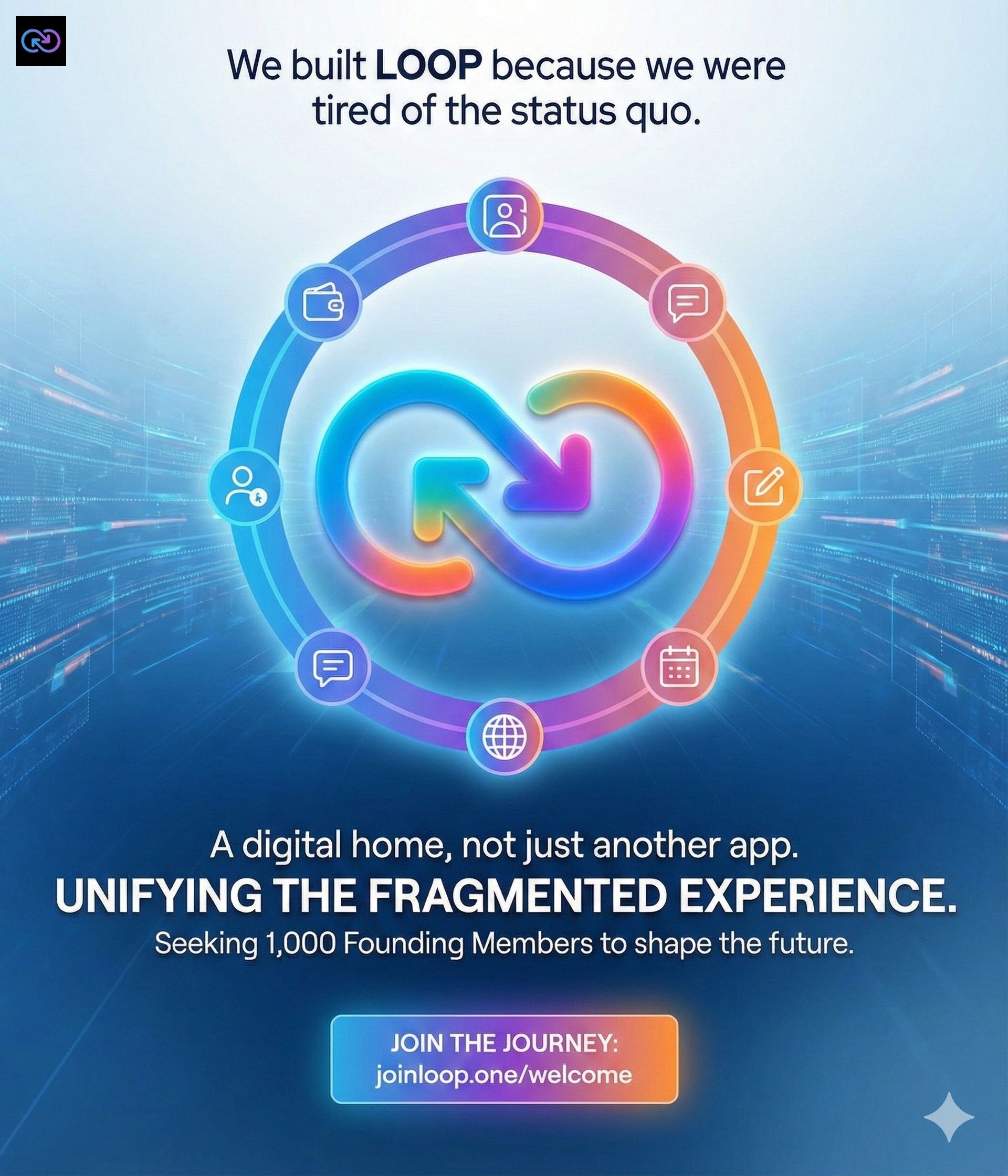

· LOOP : L’hyper-app qui rassemble tous ces services en un seul lieu.

· BreezyPay & SYNQ : Pour des paiements intelligents et intégrés.

📣 Rejoignez la Révolution

Nous lançons un mouvement :

Celui d’un or, d'un metal précieux africain numérique, juste, transparent et au service de ceux qui le produisent.

👉 Vous êtes mineur artisanal, orpailleur, coopérative, acheteur, vendeur ou acteur du secteur ?

Votre avenir commence ici :

🪙 Créez votre stablecoin avec XENN : Service XENN: https://g0a3j9zsf4x1-deploy.space.z.ai/

🌐 Tout comprendre avec LOOP, l'HyperApp :https://joinloop.one | Présentation LOOP :https://chat.z.ai/space/a0q5m87y3c20-ppt

🔥 Testez BreezyPay (Paiements e-commerce avec IA Agentique) :

🧪 Sandbox BreezyPay https://w0udp8wpzcn0-deploy.space.z.ai/

🎯 SYNQ Proof of Concept, Demo https://w0xym8zpxvw0-deploy.space.z.ai/

📊 Voyez la puissance de RISER : Pitch-Deck RISER https://chat.z.ai/space/s0q7981sm4f1-ppt

💱 Échangez sans frontières avec SWAPPIFI : Démo https://swappifidemo.space.z.ai/

💰 SWAPPIFI | Tarifs https://swappifipricing.space.z.ai/

📍 Ensemble, faisons circuler la richesse, pas les risques.

#syncgold #ornumérique #afrique #blockchain #surebanqa #swappifi #xenn #loop #empowerment #métauxprécieux #fintechafrique

Une solution SUREBANQA – Pour une Afrique financièrement autonome et souveraine.